Introduction

IRS Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, is an informational return that U.S. citizens, resident aliens, or domestic corporations with a 10% or more interest in a foreign partnership must file to report information required under Section 6038 and Section 6046A of the Internal Revenue Code. Since it is an informational filing, it does not result in additional income tax. The form helps the Internal Revenue System (IRS) enforce U.S. tax laws and prevent tax evasion by U.S. persons who are members of foreign partnerships.

You must submit Form 8865 as part of your income tax return, and the deadline is the same as the tax return’s due date. Remember, even if you’re exempt from filing an income tax return, you may still need to file Form 8865.

Key Takeaways

- Any US person with at least 10% interest in a foreign partnership must file Form 8865.

- Controlled foreign partnerships (CFPs) are those with US shareholders owning more than 50% collectively during the tax year.

- The Form 8865 filing deadline is the same as the income tax return deadline.

- Failure to submit all required information in Form 8865 will result in severe penalties.

What is Form 8865?

U.S. persons who own or control at least 10% of the total combined voting power of all classes of stock entitled to vote in a foreign partnership must file Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, to report interest, transactions, and certain activities related to foreign partnerships, as required by U.S. tax laws. The return is used to disclose information concerning controlled foreign partnerships (as required under Section 6038), transfers of property to foreign partnerships (as required by Section 6038B), acquisitions, dispositions, and changes in foreign partnership interests (as required by Section 6046A).

Controlled Foreign Partnership

When one or more U.S. shareholders own 10% or more of a foreign partnership and hold more than 50% of its interests collectively on any given day during the partnership’s tax year, the foreign partnership is classified as a controlled foreign partnership (CFP).

Why is Form 8865 Important?

U.S. persons with at least 10% interest in a foreign partnership use Form 8865 to disclose to the IRS their interests in foreign partnerships, including acquisitions and dispositions, ensuring compliance with the IRC’s reporting requirements, specifically IRC Sections 6038 and 6046A. Form 8865 also serves as a tool for the IRS to collect information about U.S. citizens’ interests and financial transactions in certain foreign partnerships, which is essential in preventing tax evasion by U.S. persons and offshore entities.

Form 8865 aids international tax enforcement efforts by facilitating information exchange between the United States and other countries. This exchange facilitates the prevention of transnational tax evasion and promotes uniformity in tax compliance worldwide. You must file Form 8865 on time to avoid hefty penalties.

Who Must File Form 8865?

Filers for Form 8865 fall into four categories. Any U.S. person who qualifies under any of the categories of filers must file Form 8865. You must complete and file a separate Form 8865 along with the applicable schedules for each foreign partnership.

Definition of U.S. Person: A U.S. person refers to any U..S citizen, resident alien, domestic entity (such as a partnership or corporation), trust under the supervision of a U.S. court or under the control of one or more US persons, or other person who is not a foreign person.

Categories of Filers:

Category 1 Filer – Any U.S. person who owned more than 50% of the partnership’s interest at any time during the partnership’s tax year.

Category 2 Filer – A U.S. person who held a 10% or greater interest in the controlled foreign partnership at any point during the foreign partnership’s tax year. If the foreign partnership had a Category 1 filer during the tax year, no one would be classified as a Category 2 filer.

Category 3 Filer – A U.S. person who contributed more than $100,000 to the foreign partnership or owned directly or constructively at least 10% interest in the foreign partnership.

Category 4 Filer – A U.S. person that had a reportable event such as acquisitions, dispositions, and changes in proportional interest (as specified in Section 6046A). A U.S. person has a reportable event if:

- Acquisition – The person in the United States did not own at least a 10% direct interest in the partnership before the acquisition, but as a result of such an acquisition, the person owned 10% or more of the partnership.

- Disposition – A U.S. person had a 10% or greater direct interest in the partnership before the disposition, and, as a result of the disposition, the person owned less than a 10% direct interest (for example, from 10% to 7%).

- Changes in proportional interests – A U.S. person has a reportable event if compared to the person’s direct proportional interest the last time the person had a reportable event, the person’s direct proportional interest has increased or decreased by at least the equivalent of a 10% interest in the partnership.

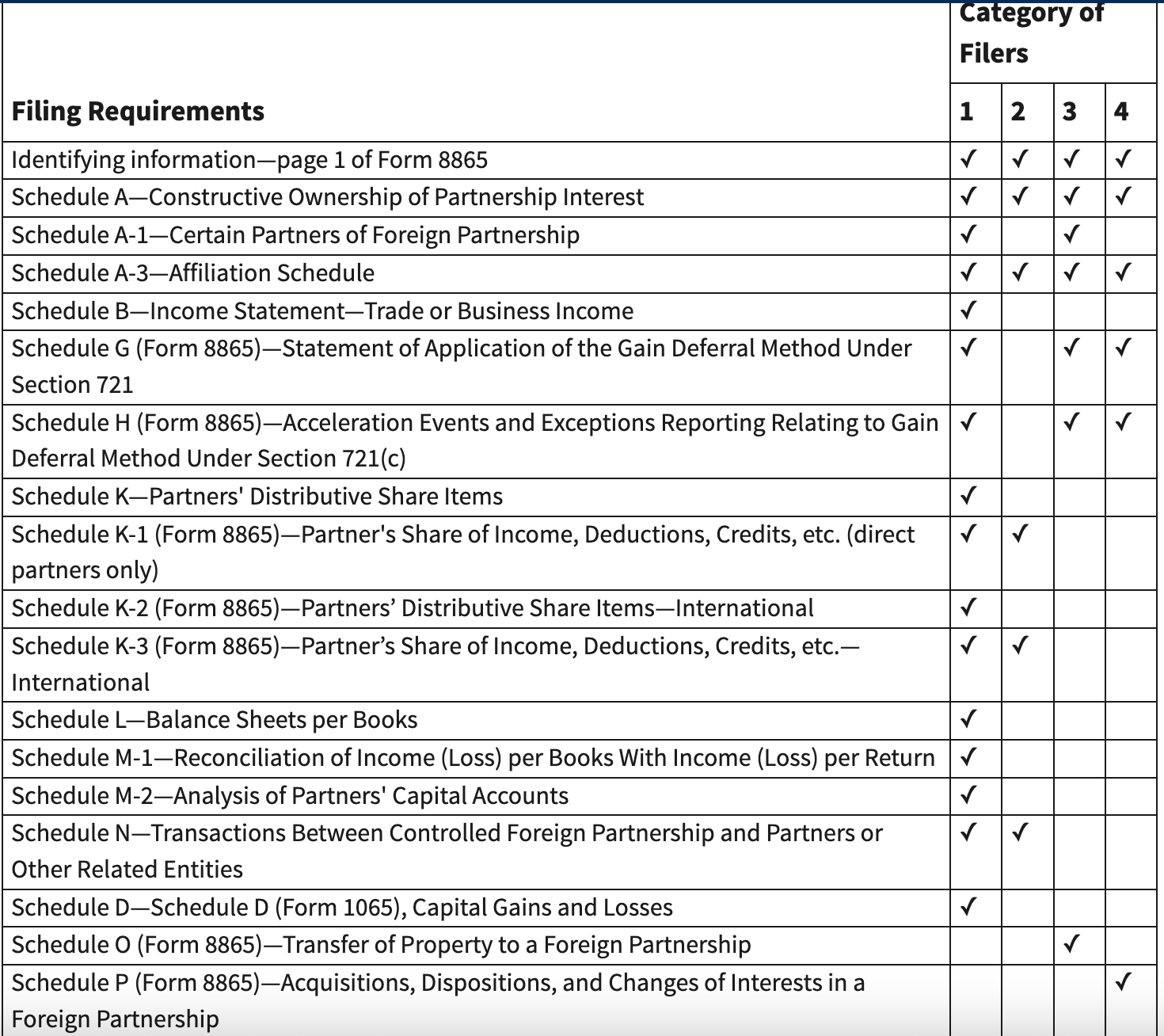

What Are the Documentary Requirements for Form 8865?

The chart below shows how the filing requirements differ based on the filer’s category. If you qualify in more than one category, you must submit all the necessary schedules for each category.

When is the Deadline for Form 8865?

Form 8865 is due at the same time as your tax return. Generally, income tax returns for U.S. citizens and residents are due on April 15. Form 4868 must be submitted no later than April 15 to request an automatic extension of time to file until October 15.

For corporations, it is due on the 15th of the fourth month following the end of the corporation’s tax year. Partnerships have until the 15th of the third month following the end of their tax year. To obtain a six-month extension, corporations and partnerships must file Form 7004 by the return’s regular due date. You may file on the following business day if the due date falls on a weekend or legal holiday.

Where is Form 8865 Filed?

File Form 8865 with your income tax return. Refer to the instructions on the form you use to file your income tax return. If you are not required to file an income tax return, you must file Form 8865 with the IRS at the same time and place as you would file an income tax return.

Where Can I Find the Newest Version of Form 8865?

The IRS website provides the latest version of Form 8865 and instructions for the form. Check back for regular updates, as many forms are updated annually at the beginning of the year.

Are There Any Penalties for Submitting an Incomplete or Late Form 8865?

If you fail to submit all the required information, the IRS may levy penalties for each year of noncompliance. Penalties may vary depending on which category you are required to file in. The penalties for each category are as follows:

Categories 1 and 2 Filers

- If you fail to provide the required information or file Form 8865 on time, the IRS will impose a $10,000 penalty for each year of each foreign partnership. After receiving the IRS Notice of Failure, you have 90 days to file the required forms. An additional $10,000 penalty (per foreign partnership) is imposed for each 30 days, or a fraction thereof, in which the failure persists after the 90 days have expired. The additional penalty is capped at $50,000 for each failure.

- Failure to provide all required information within the time frame specified will result in a 10% reduction in foreign taxes available for credit under sections 901 and 960. If the failure continues for 90 days or more after the IRS mails notice of the failure, an additional 5% reduction is made for each of the three months, or a fraction thereof, following the 90 days.

- False or fraudulent filings can result in criminal penalties.

Category 3 Filers

- The failure to properly report a contribution to a foreign partnership under Section 6038B and its regulations carries a penalty of 10% of the property’s fair market value (FMV) at the time of the contribution. This penalty is limited to $100,000 unless the failure was intentional.

Category 4 Filers

- Any person who fails to properly report all the information requested by Section 6046A is subject to a $10,000 penalty, in addition to the Section 7203 criminal penalty, unless it can be demonstrated that such failure is due to reasonable cause. If the failure continues for more than 90 days after the IRS mails notice of the failure, an additional $10,000 penalty will apply for each 30-day period (or fraction thereof) during which the failure continues after the 90-day period has expired. The additional penalty shall not exceed $50,000.

Need Help with Filing Form 8865?

Cleer Tax is here for you! Business owners find it extremely stressful to manage their businesses and pay their taxes. “The hardest thing in the world to understand is income tax,” as Albert Einstein famously observed. At Cleer, you don’t have to worry about your taxes because we are here to help. Our experienced accountants can handle your Form 8865 so that you can focus on managing your business.

Because there are severe penalties for incorrectly filling out this form, it is risky to prepare it without subject-matter expertise. If your company is required to file this form, we can do so for a small, flat fee to keep you from incurring fines that cost an arm and leg. The Cleer Tax experts provide Federal Income tax preparation services, which includes your Form 8865. We also offer comprehensive all-in-one monthly accounting packages that include monthly statements as well as your federal and state tax returns. If you have any questions about filing this form or other filing requirements, schedule a consultation to discuss it further.

If you need help finding the right tax prep or bookkeeping package, email our customer success team at hello@cleer.tax