Introduction

As John Maynard Keynes famously remarked, “The avoidance of taxes is the only intellectual pursuit that carries any reward.” A company and its stakeholders do stand to benefit from the strategic management of taxes through legal means. The IRS provides businesses with various remedies and options to help them navigate their tax obligations more effectively. Companies can reduce their tax obligations by understanding the applicable tax laws and selecting the most advantageous options. One such option is to file Form 2553 to elect to be taxed as an S-corporation, which eliminates double taxation and can result in substantial tax savings.

Key Takeaways

- A corporation or entity must meet all requirements to be eligible for S-corporation status.

- Form 2553, Election by a Small Business Corporation, enables eligible entities to choose S-corporation status under Section 1362(a) of the tax code. This election shifts the tax burden from the corporation to the shareholders, potentially avoiding double taxation.

- Form 2553 must be filed within two months and 15 days after the start of the tax year in which S-corporation status is desired or at any time during the preceding tax year.

- It cannot be filed electronically; it must be mailed or faxed to the appropriate IRS center. You may also use private delivery services.

- Late filing relief may be available under IRS Revenue Procedure 2013-30 if certain conditions are met, but it must be requested within a specified timeframe.

What is Form 2553?

Form 2553, Election by a Small Business Corporation, is used by a corporation or other eligible entity to elect to become an S-corporation under Section 1362(a). An eligible entity that meets specific criteria will be treated as a corporation as of the S-corporation election’s effective date and is not required to file Form 8832, Entity Classification Election.

Corporations are taxed as C-corporations by default unless they elect to be taxed as S-corporations. Under S-corporation status, income is taxed to the shareholders rather than the corporation. One reason C-corporations elect to be taxed as S-corporations is to avoid double taxation. In C-corporations’ case, the business’s income is subject to federal income tax at the entity level. On the other hand, when profits are distributed to shareholders in the form of dividends, those dividends are subject to taxation once more at the level of the individual shareholder as personal income.

Who Has to File Form 2553?

A corporation or other entity is eligible to elect to be taxed as an S-corporation if it meets the following criteria:

- It must be a domestic corporation or entity.

- It has at most 100 shareholders. Individuals and their spouses (estates) are treated as one shareholder. All members of a family (as defined in Section 1361(c)(1)(B)) and their estates are considered to be one shareholder.

- Its shareholders must be individuals, estates, specific exempt organizations, or certain trusts described in Section 1361(c)(2)(A).

- It has no nonresident alien shareholders. This means that shareholders should be US citizens or resident aliens.

- It has only one class of stock.

- It must not be an ineligible corporation, such as a bank, an insurance company subject to tax under subchapter L of the Internal Revenue Code (IRC), a domestic international sales corporation (DISC), or a former DISC.

- It has or will adopt or change to one of the following tax years:

- A tax year ending December 31

- A natural business year

- An ownership tax year

- A tax year elected under Section 444

- A 52-53-week tax year ending with reference to a year listed above

- Any other tax year (including a 52–53-week tax year) for which the corporation (entity) establishes a business purpose

- Each shareholder must consent to S-corporation status.

If these conditions are met, the entity can elect to be treated as an S-corporation without filing Form 8832.

When is Form 2553 Due?

Form 2553, used to make an election to be treated as an S-corporation, must be completed and filed within specific timeframes.

- The election must be made no later than two months and fifteen days after the start of the tax year in which the S-corporation status will take effect.

Note: The 2-month period starts on the first day of the tax year and concludes at the end of the day, corresponding to the same numerical day in the second calendar month following that month. If there is no corresponding day, the period ends on the last day of that second calendar month. For example, the beginning of the year when the S-corporation is elected is January 1, 2023, and the due date of filing is March 15, 2023.

- Form 2553 can be filed at any time during the tax year immediately preceding the tax year in which the S-corporation status is intended to take effect. For example, if the election of an S-corporation takes effect in 2024, it may be filed at any time in 2023.

Essentially, the entity must adhere to these timeframes to ensure the timely and effective filing of Form 2553 for S-corporation election.

Where is Form 2553 Filed?

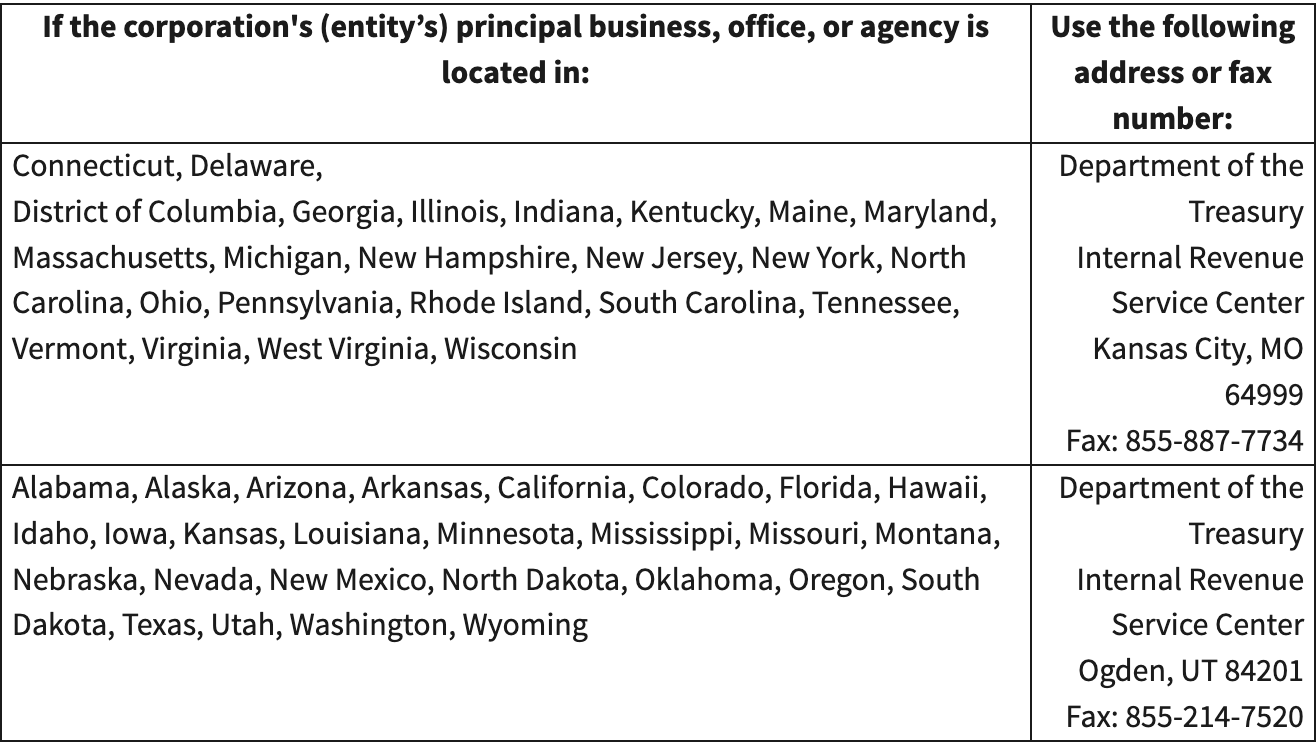

Form 2553 cannot be filed online. You may refer to the diagram below to find out where to mail or fax the form. If you choose to fax it, keep the original copy for your records.

You can also use private delivery services (PDS) designated by the IRS. Visit IRS.gov/PDS for the list of designated services. For the IRS mailing address when using PDS, visit IRS.gov/PDSStreetAddresses.

Where Do I Find the Newest Version of Form 2553?

The IRS website provides the newest version of Form 2553 and instructions. Check back for regular updates, as many forms are updated annually at the beginning of the year.

Is There a Penalty if Form 2553 is Not Filed or Filed Late?

Filing Form 2553 is not mandatory. The IRS does not impose penalties for non-filing or failing to file the form to elect the S-corporation tax classification in the appropriate timeframe. On the other hand, if you do not file Form 2553, it is likely that your company will not be granted S-corporation status in the subsequent tax year unless you are eligible for late election relief.

For example, due to the late filing of Form 2553, the corporation will default to being taxed as a C-corporation, which means it will be subject to regular corporate income tax rules. A corporation that intended to elect S-corporation status but failed to do so at an appropriate time may miss out on the tax benefits associated with S-corporation tax classification, such as pass-through taxation and the avoidance of double taxation on dividends.

If Form 2553 is filed after the deadline, the entity may request relief under the late election relief procedures in IRS Revenue Procedure 2013-30. The revenue procedure outlines four requirements the corporation must meet to be eligible for relief:

- The entity intended to be classified as an S-corporation is an eligible entity and failed to qualify as an S-corporation solely because the election was not timely.

- The entity has reasonable cause for failing to make the election timely.

- The entity and all shareholders reported their income consistent with an S-corporation election in effect for the year the election should have been made and all subsequent years.

- Less than three years and 75 days have passed since the effective date of the election.

Can Cleer Tax Help Me with Filing Form 2553?

Absolutely! At Cleer Tax, our dedicated team is committed to addressing the distinct requirements of your business. We provide comprehensive tax advisory services tailored to your specific needs, covering every aspect of compliance and optimization. Our goal is to ensure that you capitalize on every available opportunity, leaving no stone unturned when maximizing your tax benefits and minimizing any potential liabilities.

CLEER provides Corporate Income Tax Packages encompassing federal and state income tax filings for a hassle-free experience. Our comprehensive new company package offers tax consultation, bookkeeping, and a chart of accounts set up to help you do it right from the start. We also offer all-in-one monthly accounting packages, which include your monthly statements plus your federal and state tax returns

If you have any questions about filing Form 2553 or other filing requirements, schedule a consultation to discuss them further. You may also email Customer Success at hello@cleer.tax.