According to U.S. tax rules, a disregarded entity is a business entity (a limited liability company (LLC) or a single-member limited liability company (SMLLC)) that is treated as transparent for tax purposes. The entity itself is not taxed. Instead, its income, deductions, and credits flow to its owner(s), who report them on their tax returns. Essentially, for tax purposes, the entity is disregarded, and its activities are treated as if they were directly conducted by the owner.

Before 2018, foreign-owned U.S. disregarded entities had no tax filing obligations. Income was subject to U.S. tax if it came from engaging in a U.S. trade or business (ETBUS). Merely having a U.S. LLC does not make income ETBUS if you’re based outside the U.S.

Key Takeaways:

- Since 2018, foreign-owned U.S. disregarded entities are required to file two forms: Form 5472 (Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business) and Form 1120 (U.S. Corporation Income Tax Return). Form 5472 and Form 1120 provide detailed information about the entity’s transactions and basic information to the IRS (Internal Revenue Service).

- Foreign owners must determine if their income qualifies as Effectively Connected with a U.S. Trade or Business (ETBUS) income. Having a U.S. LLC alone doesn’t automatically make income ETBUS; it depends on factors like location, business activities, and presence of employees or property in the U.S.

- Failing to file the required forms on time can lead to substantial penalties. The penalty for a late or inaccurate Form 5472 can be as high as $25,000.

- Although foreign-owned U.S. disregarded entities might not have a tax liability due to filing these forms, compliance is crucial. The penalties for non-compliance can be severe, potentially impacting your business operations and financial stability.

What are Foreign-Owned U.S. Disregarded Entities?

A Foreign-Owned Disregarded Entity (FODE) refers to a legal entity owned by foreign individuals or entities and classified as a “disregarded entity” for U.S. federal tax purposes. In this context, “foreign” refers to individuals or entities that are not considered residents or citizens of the United States.

What are the Tax Filing Requirements for Foreign-Owned U.S. Disregarded Entities?

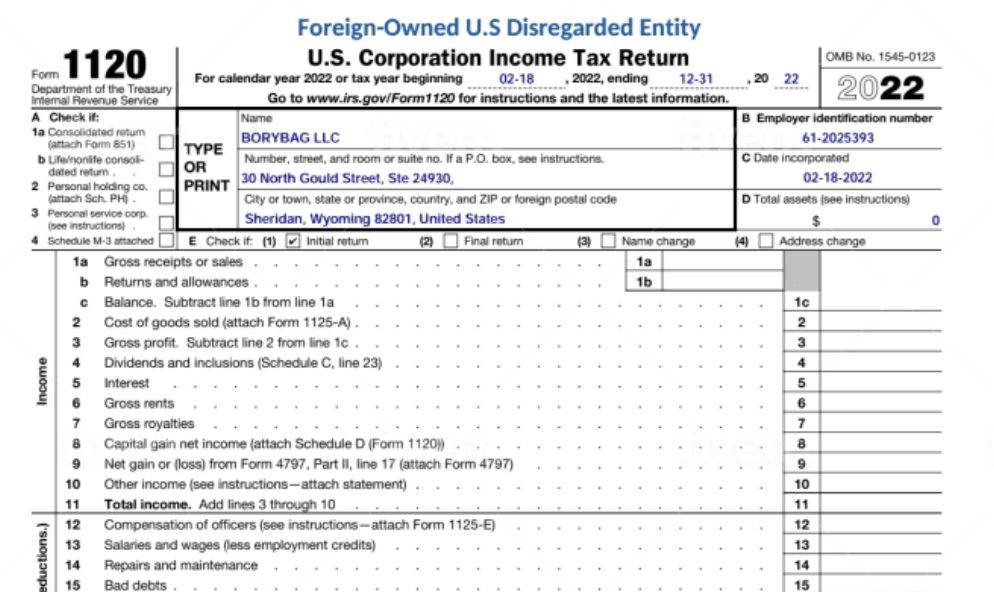

As of 2018, foreign-owned U.S. disregarded entities must file Form 5472 and Form 1120. Due by April 15, they can be extended to October 15 with Form 7004, the Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns. Form 1120 (U.S. Corporation Tax Return) doesn’t imply tax liability; it only gathers basic info. Form 5472 provides more detailed info, mainly reporting transactions between the owner and LLC.

What is Form 5472?

Form 5472 is a U.S. tax form used to report transactions between certain FODEs, foreign corporations engaged in a trade or business within the U.S., and related parties. The purpose of Form 5472 is to provide the IRS with information about these transactions to ensure proper taxation and to prevent tax avoidance or evasion through intercompany transactions.

Key Points about Form 5472:

- If foreign-owned U.S. disregarded entities or foreign corporations that are engaged in a trade or business within the U.S. have reportable transactions with a related party (another entity that is closely connected, such as through ownership or control), Form 5472 must be filed.

- Form 5472 requires the disclosure of financial and transactional information for each related party involved in reportable transactions. This information includes details about the nature of the transaction, the amounts involved, and any additional relevant information.

- Form 5472 is typically filed as an attachment to the filer’s annual U.S. income tax return, whether it’s an individual tax return (Form 1040, U.S. Individual Income Tax Return) or a business tax return (such as Form 1120 or Form 1065, U.S. Return of Partnership Income).

- Failure to file Form 5472 or filing an incomplete or incorrect form can result in penalties imposed by the IRS.

What are the Reportable Transactions in Form 5472?

Reportable transactions on Form 5472 refer to certain types of transactions and activities that must be disclosed when filing the form. These transactions generally involve payments or financial dealings between a FODE, a foreign corporation engaged in a U.S. trade or business, and related parties. The purpose of reporting these transactions is to provide transparency to the U.S. tax authorities (IRS) and prevent tax avoidance or evasion through inter-company transactions.

Here are some examples of reportable transactions that may need to be disclosed on Form 5472:

- Sales and Purchases of Goods and Services: Transactions involving the sale or purchase of goods, products, or services between the foreign-owned entity and related parties.

- Loans and Advances: Loans or financial advances made between the entity and related parties, including interest rates, terms, and repayment details.

- Royalties and Licensing Fees: Payments for the use of intellectual property (such as patents, copyrights, and trademarks) between the entity and related parties.

- Rental and Lease Payments: Rental or lease payments for property or equipment between the entity and related parties.

- Management and Administrative Services: Payments for management, administrative, or consulting services provided by or to the entity and related parties.

- Cost-Sharing Agreements: Transactions related to cost-sharing arrangements where the entity and related parties jointly share the costs and risks of developing, producing, or obtaining intangible property.

- Interest Payments: Interest payments on loans or financial instruments between the entity and related parties.

- Research and Development Payments: Transactions involving research and development expenses between the entity and related parties.

- Insurance Premiums: Payments of insurance premiums between the entity and related parties.

Are There Penalties for Not Filing the Required Forms as a Foreign-Owned U.S. Disregarded Entity?

Filing the above-mentioned forms incurs no tax, but not filing results in severe penalties for foreign-owned U.S. disregarded entities. Missing the accurate Form 5472 deadline can lead to a $25,000 penalty.

Can Cleer Tax Help with the Tax Requirements for Foreign-Owned U.S. Disregarded Entities?

YES! Cleer not only ensures tax filing compliance for foreign-owned U.S. disregarded entities, but also compliance with state tax and Delaware Franchise Tax.

Cleer provides accurate, affordable, and efficient financials and tax services for U.S. businesses and subsidiaries to help entrepreneurs do it right from the start. We offer tax services from preparation to filing, including for Foreign-Owned Disregarded Entities and Form 5472. Once all financial statements and necessary documentation are provided to us, we can start preparing the form. After Form 5472 is drafted, it will be reviewed by our internal tax reviewers before sending it to you for review. Form 8879, IRS e-file Signature Authorization, will be provided for signature to allow us to e-file Form 1120 on your behalf.