Reconciliation in accounting is akin to investigative work in the financial world. It’s a process that compares two sets of records to make sure everything adds up correctly. It functions as a financial detective, verifying your financial accounts’ accuracy, consistency, and completeness. Reconciliation serves as a safeguard against errors, discrepancies, and even potential fraud by ensuring that all transactions are correctly recorded. It is like a monthly checkup for your financial health, ensuring your transactions are properly recorded. Reconciliation in accounting is, in essence, a sound business practice that guarantees the accuracy of your financials.

Although the procedure is not set in stone, it often involves comparing your internal records to external ones, like bank reports and payroll documents.

Key Takeaways

- Reconciliation in accounting verifies and validates the consistency and correctness of financial records.

- Reconciliation usually involves comparing internal records with external ones, such as bank statements.

- Reconciliation is essential for preventing financial errors, detecting fraud, and maintaining good standing with auditors.

- Make sure everything matches up, and keep those supporting documents handy.

- Reconciliation is one of the best practices for ensuring your financials are accurate and reliable.

What is Reconciliation in Accounting?

- Reconciliation in accounting verifies that the numbers are accurate and consistent by comparing two sets of records.

- It verifies the general ledger’s accounts’ accuracy, consistency, and completeness.

- It detects fraud and prevents financial account errors and unexplained discrepancies.

Let Us Take a Look at How Reconciliation Works:

There is no set format for reconciliation in accounting. However, GAAPs (Generally Accepted Accounting Principles) require double-entry accounting. Transactions are recorded in the general journal in two locations: debit and credit. Using this can help detect errors on either side of the entry. Debits and credits in an account reconciliation should equal zero.

When it comes to the two accounts, one will be recorded as a debit and the other as a credit.

For example:

- Purchasing supplies results in a debit to supplies (shown on the income statement) and a credit to cash or accounts payable (shown on the balance sheet) for the business owner.

Supplies xxx

Cash/Accounts Payable xxx

- A company’s balance sheet shows cash or accounts receivable as a debit when a sale is made, while the income statement shows sales revenue as a credit.

Cash/Accounts Receivable xxx

Sales Revenue xxx

Why Do We Need Reconciliation in Accounting?

Any business that wants to detect fraud, avoid negative audit opinions, and prevent balance sheet errors must use reconciliation. Once a month, bookkeepers typically reconcile the sheets. Making sure that transactions are accurately booked into the appropriate general ledger account requires reviewing each account on the balance sheet.

Adjusting entries is required if transactions were booked incorrectly. For example, when we reconcile bank accounts, we may refer to the monthly generated bank reports to make sure that all the transactions are booked in that particular month before we can continue recording the transactions for the succeeding months. The supporting documents are extremely important when reconciling; we must ensure we use the correct and updated supporting documents. One smart business move that can help an organization’s growth is reconciliation.

Process of Reconciliation in Accounting

Reconciliation in accounting involves comparing and verifying financial records to ensure accuracy, consistency, and completeness. It is a critical step in the accounting process that helps detect discrepancies, errors, and fraud. This entails comparing the internal and external accounts, reviewing source documents like bank reports (payments and deposits) and payroll reports, taking notes of charges or expenses that have no receipts, and making sure that all the recorded debits match the credits.

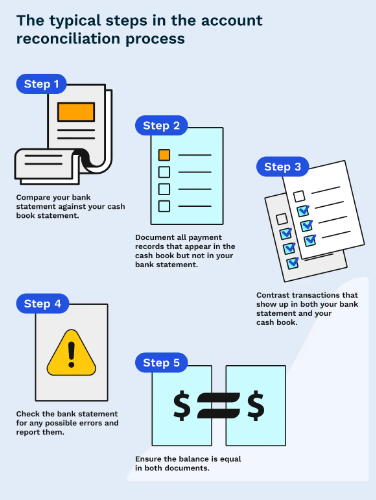

Here’s a general outline of the steps involved in bookkeeping reconciliation:

1. Gather Documentation: Collect all relevant financial documents, such as bank statements, receipts, invoices, and other supporting records.

2. Identify Accounts to Reconcile: Determine which accounts must be reconciled. Bank accounts, credit card accounts, accounts receivable, and accounts payable are commonly reconciled.

3. Compare internal and external records: Compare the transactions entered in the company’s books to external documents like bank statements or vendor invoices. Ensure that the dates, amounts, and transaction descriptions are consistent between internal and external records.

4. Verify Balances: Calculate the account’s ending balance based on the company’s records. Compare this balance with the ending balance shown on the external records (e.g., bank statement).

5. Identify Discrepancies: If there are discrepancies between the internal and external records, investigate the reasons for these discrepancies. Common causes include:

- Outstanding checks or deposits that the bank still needs to clear

- Errors in recording transactions.

- Unauthorized or fraudulent transactions.

- There are timing differences between when transactions are recorded in the company’s books and when they appear in external records.

6. Make Adjustments: If errors or discrepancies are found, make the necessary adjustments in the company’s books to reconcile the accounts. This may involve correcting entries, recording missing transactions, or addressing unauthorized or fraudulent activity.

7. Review Supporting Documents: Ensure that all supporting documents, such as receipts, invoices, and bank statements, are accurate and up-to-date. Retain these documents for auditing and compliance purposes.

8. Document the Reconciliation Process: Maintain clear and detailed documentation of the reconciliation process, including the steps taken, adjustments made, and any issues that were resolved. Documenting the process helps provide a clear audit trail and ensures transparency.

9. Repeat Regularly: Reconciliation should be performed regularly, oftentimes on a monthly basis, for critical accounts, such as bank accounts. Regular reconciliation helps detect errors and discrepancies early, preventing them from accumulating.

10. Reporting: Prepare reconciliation reports and summaries that detail the findings and adjustments made during the reconciliation process. These reports can be helpful for management, auditors, and financial stakeholders.

11. Continuous Improvement: Continuously assess and improve internal controls and accounting procedures to reduce the likelihood of reconciliation issues in the future. The steps and procedures for reconciling accounts vary depending on the type of account and the company’s industry. Additionally, following generally accepted accounting principles (GAAPs) or other relevant accounting standards is essential to ensuring accurate and compliant bookkeeping reconciliation.

Can Cleer Tax Help Me Reconcile my Books, Maintain Accurate Records, and Prepare my Financial Statements?

Absolutely! U.S. businesses and their subsidiaries can rely on Cleer Tax for efficient, accurate, reasonably priced bookkeeping and tax services to simplify reconciliation in accounting. Cleer offers a new company package that includes a tax consultation, bookkeeping, and a chart of accounts set up to help you do it right from the start. We have all-in-one monthly accounting packages that include not only your federal and state tax returns, but also your monthly statements. We also provide federal income tax preparation, which includes your state taxes, to help you file correctly with the IRS.

Have additional questions? Book a consultation or contact us and let our team of tax professionals take care of your needs.